In 2026, small business risks have shifted significantly. While a simple “General Liability” policy used to be the gold standard, the rise of sophisticated cyber threats, supply chain instability, and a changing labor market has made insurance a strategic necessity rather than just a “check the box” expense.

The good news? The commercial insurance market in 2026 is finally softening. Rates are stabilizing or even dropping in many sectors as insurers compete for your business.

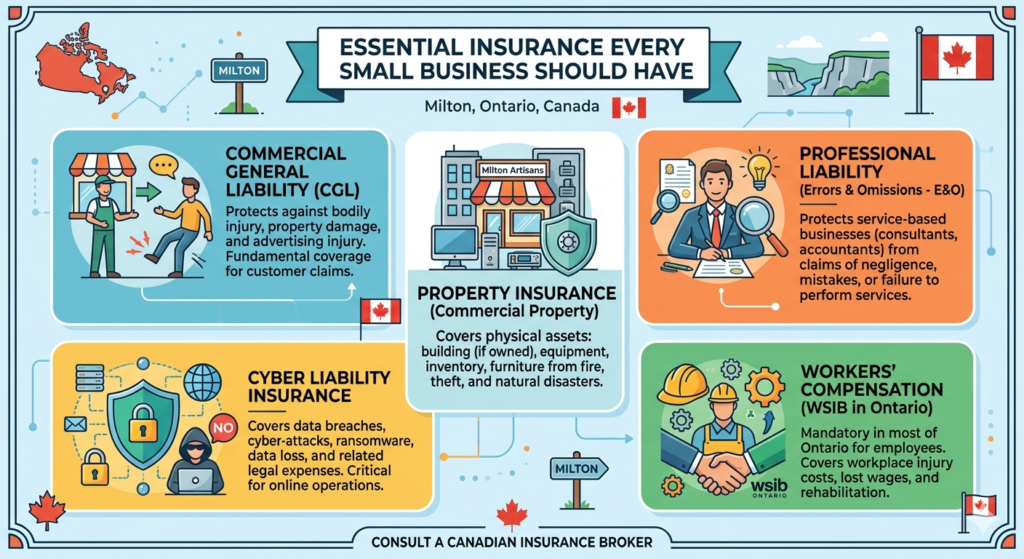

Here is the essential breakdown of the insurance every small business should have this year to stay protected and competitive.

1. Commercial General Liability (CGL)

Often called “slip and fall” insurance, CGL is your first line of defense. It covers third-party bodily injuries and property damage occurring on your premises.

- Why it’s vital in 2026: Legal costs and settlements are rising. Most experts recommend a minimum limit of $2 million to ensure you aren’t paying out of pocket for a single unfortunate accident.

2. Cyber Liability Insurance

In 2026, cyber insurance has moved from “optional” to “non-negotiable.” Small businesses are now primary targets for AI-driven phishing and ransomware attacks.

- What it covers: Data breach recovery, legal fees, notifying affected customers, and even “social engineering” fraud (where hackers trick you into transferring funds).

- Pro Tip: Many insurers now require you to have Multi-Factor Authentication (MFA) and employee training in place just to qualify for a policy.

3. Business Interruption Insurance

If a fire or natural disaster forces you to close your doors for a month, how do you pay your rent and staff?

- The 2026 Edge: Modern policies are increasingly covering supply chain disruptions. If your primary supplier is shut down by a disaster and you can’t operate, this coverage can help replace your lost income.

4. Professional Liability (Errors & Omissions)

If your business provides advice, consulting, or specialized services, CGL isn’t enough. You need E&O to protect against claims of negligence or failure to deliver a promised service.

- Who needs it: Consultants, IT providers, accountants, and even specialized trades.

- The Risk: A simple mistake in a project could lead to a client losing thousands—and they will look to you to bridge that gap.

5. Workers’ Compensation (WSIB in Ontario)

Protecting your team is both a legal and moral obligation. In Ontario, for example, 2026 has seen a drop in premium rates (averaging $1.23 per $100 of payroll), making it more affordable than in previous years.

- Modern Twist: With hybrid and remote work now the norm, ensure your coverage accounts for employees working from home or in different provinces/states.

2026 Quick Comparison Table

| Insurance Type | Primary Protection | 2026 Trend |

| General Liability | Physical accidents/injuries | Rates are flat; focus on higher limits. |

| Cyber Liability | Data breaches & AI scams | Essential; insurers demand better security. |

| Business Interruption | Lost income during downtime | Now often includes supply chain issues. |

| Professional Liability | Mistakes in service/advice | Critical for service-based “Solopreneurs.” |

| Commercial Auto | Business vehicle accidents | Rates are rising due to high repair costs. |

Export to Sheets

The “2026 Audit” Checklist

Don’t just renew your old policy. Ask your broker these three questions:

- “Does my property limit reflect 2026 market values?” (Inflation has likely made your equipment more expensive to replace than it was two years ago).

- “Am I eligible for a ‘soft market’ discount?” (Competition is high—use it to your advantage).

- “Does my cyber policy cover AI-generated fraud?”

The Bottom Line: Insurance shouldn’t just address today’s accidents; it should anticipate tomorrow’s disruptions. By bundling these coverages, you aren’t just buying a policy—you’re buying the ability to stay in business when things go wrong.

Would you like me to draft a customized “Risk Assessment” email you can send to your insurance broker to see if you’re overpaying?